SEC Adopts Narrower Version of Dealer Registration Rules

SEC Adopts Narrower Version of Dealer Registration Rules

SEC Adopts Narrower Version of Dealer Registration Rules

Earlier today, the Securities and Exchange Commission in a 3‑2 vote adopted new Rules 3a5‑4 and 3a44‑2 (together, the Dealer Rules) under the Securities Exchange Act of 1934, as amended (the Exchange Act), that will define who is deemed to be buying and selling securities as a regular part of its business and thus considered a “dealer” or “government securities dealer.”1

Existing Definition

Section 3(a)(5) of the Exchange Act generally defines a “dealer”2 as “any person engaged in the business of buying and selling securities . . . for such person’s own account through a broker or otherwise.” The definition, however, provides an important exclusion from the dealer definition for any persons who buy or sell securities for their own account but “not as a part of a regular business.”

Market participants have relied on the above exception to view investment funds and other entities that frequently “trade” securities to not be “dealers” that have to register with the SEC or become a member of the Financial Industry Regulatory Authority (FINRA).

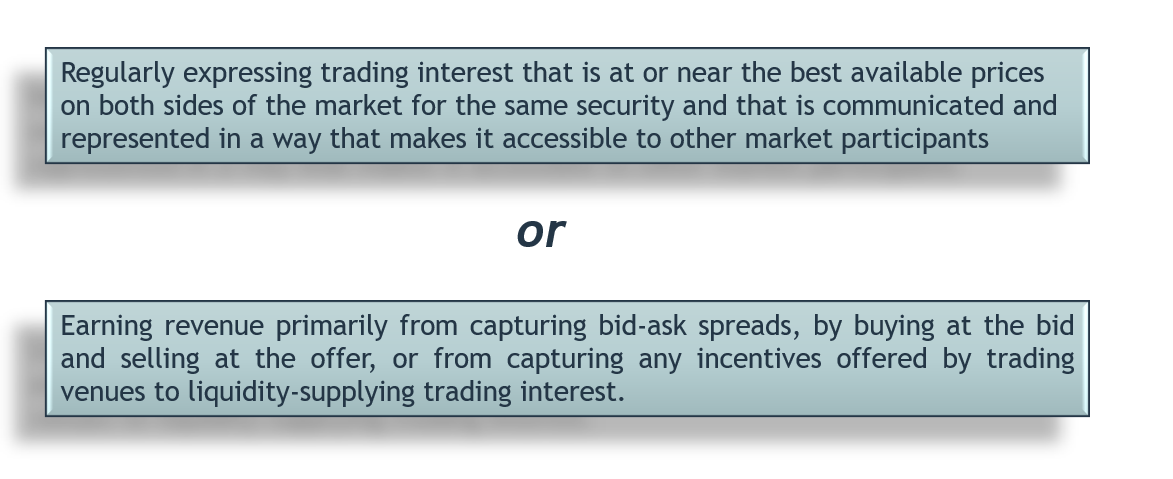

Dealer Rules Revisions

The Dealer Rules narrow the above exception by establishing two qualitative standards that would constitute dealing “as part of a regular business.” Specifically, the Dealer Rules provide that a person buying and selling securities “for its own account” is engaged in that activity “as a regular business” if that person engages in a regular pattern of buying and selling securities that has the effect of providing liquidity to other market participants by:

The Dealer Rules specifically define “own account” as any account held in the name or for the benefit of the applicable person.

The Dealer Rules, however, specifically exclude any persons who have or control total assets of less than $50 million; registered investment companies; or central banks, sovereign entities or international financial institutions (as defined in the Dealer Rules).

Key Takeaways

The SEC included an “expansion clause” (our terms) in the Dealer Rules, noting that “no presumption shall arise that a person is not a dealer . . . solely because that person does not satisfy [the Dealer Rules’ requirements.]” As a result, even if a person, adviser or fund gets comfortable that it does not fall within the narrower interpretation of engaging in activity as a part of a regular business, the SEC could always make a determination that such person is nevertheless a dealer under the Exchange Act.

There is no specific exclusion in the Dealer Rules for registered investment advisers or their private funds. The Dealer Rules’ adopting release notes that hedge funds are more likely to meet the final rules’ definition of dealing, although private equity funds and liquidity funds are less likely. In light of the uncertainty regarding the application of the Dealer Rules, investment advisers will need to carefully review their trading and other activities to determine whether they or the funds they manage engage in activity covered by the qualitative standards “as a part of a regular business” or whether they or the funds they manage could otherwise be perceived by the SEC as a dealer.

1 The Dealer Rule will become effective 60 days after the adopting release is published in the Federal Register, with a compliance date one year after the effective date.

2 The definition of “government securities dealer” in Section 3(a)(44) of the Exchange Act is materially similar to the definition of “dealer” in Section 3(a)(5). This alert primarily discusses the changes to the “dealer” definition, although the final rule includes similar changes to the definition of “government securities dealer.”