2026 Perspectives in Private Equity: Defense & National Security

This article is part of the “Perspectives in Private Equity” series.

One of the hottest areas for escalating private equity investment in 2025 was the defense industry, as buyout firms that had traditionally steered clear of an industry fraught with both geopolitical and public perception risk sensed a growing opportunity.

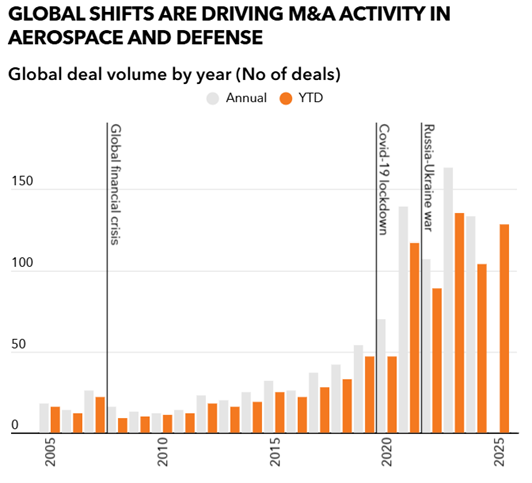

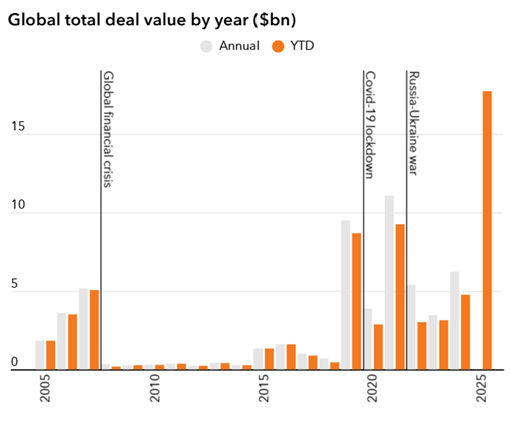

Year-to-date data published by PE Hub in November 2025 showed the year already exhibiting record-breaking deal activity, with private equity and venture capital spending on aerospace and defense assets standing at $17.7 billion versus a previous full-year record of $11 billion in 2021.

Source: PE Hub

Drivers of Defense Investing

Several drivers are fueling the flurry of investment, beyond the outbreak of conflicts in Ukraine, Gaza and elsewhere that appeared to kickstart the latest deal uptick. With technological innovation a key feature of the sector, the creation of next generation capabilities in defense technology and munitions are driving a lot of activity. We see a lot of fast-growing venture capital targets in both the start-up and spin-out space and expect momentum to continue building there.

Further, large conglomerates experiencing high demand are focusing on core priorities and divesting assets that present compelling openings for private equity buyers capable of executing complex carve-outs. We also see traditional primary defense contractors partnering with minority stake investors and entering joint ventures to tap private funds and capitalize on the opportunities in front of them.

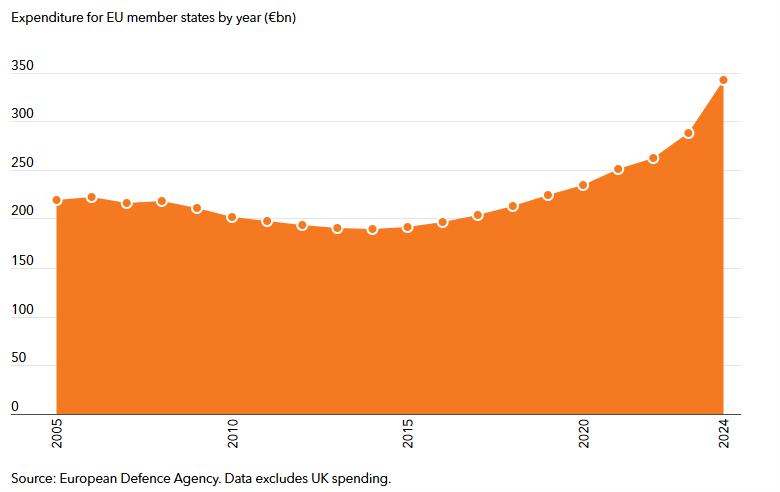

Finally, questions over the reliability of the United States as a partner in global alliances are forcing a worldwide reckoning over defense budgets, driving significant national investment programs across Europe, the Middle East and beyond. A re-arming effort by several European nations, along with NATO, is gathering momentum while countries like Saudi Arabia and the United Arab Emirates look to build their own militaries and similar themes are evident in Asia. That rise in defense spending is creating new investment opportunities for funds.

The Rise of EU Defense Spending

Source: PE Hub

Some of the other segments of the aerospace and defense industry that we see attracting increasing interest include disruptors like unmanned aerial vehicles, satellites and the space economy and defense tech encompassing AI, autonomy, cyber and mission software.

In all of these areas, private equity funds butt up against national security concerns when they look to execute deals. Cross-border transactions in other hot areas like semi-conductors, digital infrastructure, shipping, AI and cloud computing are also facing much greater scrutiny as the definition of national security shifts and countries weigh up the risks associated with foreign investment in their most sensitive industries.

Navigating National Security Complexities

Trade tensions between the United States and several countries, including China and Russia, have existed for many years as their differing world views have been judged to be in conflict with U.S. interests. The approach of the new administration has shifted the landscape on national security, however, with President Trump having made clear throughout his campaign that he intended to take a different view of the meaning of national security and how it should be protected.

Since taking office, the new administration has sought to more closely link national security goals to trade policy, with tariffs in particular seen as a key lever in furthering U.S. objectives. The government has also shown a willingness to take equity stakes in companies that it believes have a critical role to play in safeguarding American interests. In September, the Trump administration secured a roughly 10% stake in Intel, acquired via CHIPS and Science Act funding, to revive domestic semiconductor manufacturing, for example. Further, the President has entered into new alliances with countries including Saudi Arabia as his administration adopts a more proactive approach to directing capital flows in sensitive industries.

For private equity, this new backdrop creates plenty of investment opportunities around the globe but calls for careful navigation. Many of the opportunities – in data centers, digital infrastructure, aerospace, defense tech and beyond – are subject to intense scrutiny from both an outbound and inbound perspective. Funds must be alive not only to the complex international web of applicable controls and policies, but also to the prospect of deep government questioning of investors, partnerships, customers and supply chains.

Transacting in sectors deemed sensitive from a national security perspective calls for a higher level of diligence, compliance and structuring, covering everything from where an operating company is incorporated to who is on the board and whether LPs from certain countries can participate. Given booming deal volumes, many private equity firms are now prioritizing efforts to strengthen their knowhow, systems and procedures in order to participate.