2026 Perspectives in Private Equity: Evolution of Financing Sources

This article is part of the “Perspectives in Private Equity” series.

With deal activity improving gradually through 2025, private equity funds keen to deploy capital and control portfolio company costs drove several months of record repayments on leveraged loans and historically high levels of dividend recapitalizations.

In a particularly dynamic financing market, the combination of rate cuts, measured inflation and resilient equity markets provided more certainty on pricing and led to financing costs coming down. Private capital faced more competition from traditional bank lenders in the acquisition financing space given lower deal volumes, but its ability to provide capital structure flexibility saw it dominate refinancings and recapitalizations.

With significant dry powder available, the secular trends underpinning the growth of direct lending show no signs of weakening and private credit continues to build its market share, particularly in the mid-market. Given their ability to provide borrowers certainty and speed of execution, alongside long-term, flexible and supportive capital, direct lenders have stepped up as constructive partners in recent challenging market conditions and we expect their position to only strengthen going forward.

All finance providers will look back on the past 12 months as notable for the growing prevalence of asset-backed lending and the widespread use of junior debt capital, payment-in-kind structures, annual recurring revenue loans and the bespoke financing solutions for distressed borrowers.

Among the sectors that were the most active, and look set to be so in the year ahead, we saw a lot of appetite among lenders for supporting technology, energy, mining, utilities, financial services and health care deals. Many of these areas look set to benefit from the advance of artificial intelligence, and we expect increased volumes to remain a trend for 2026.

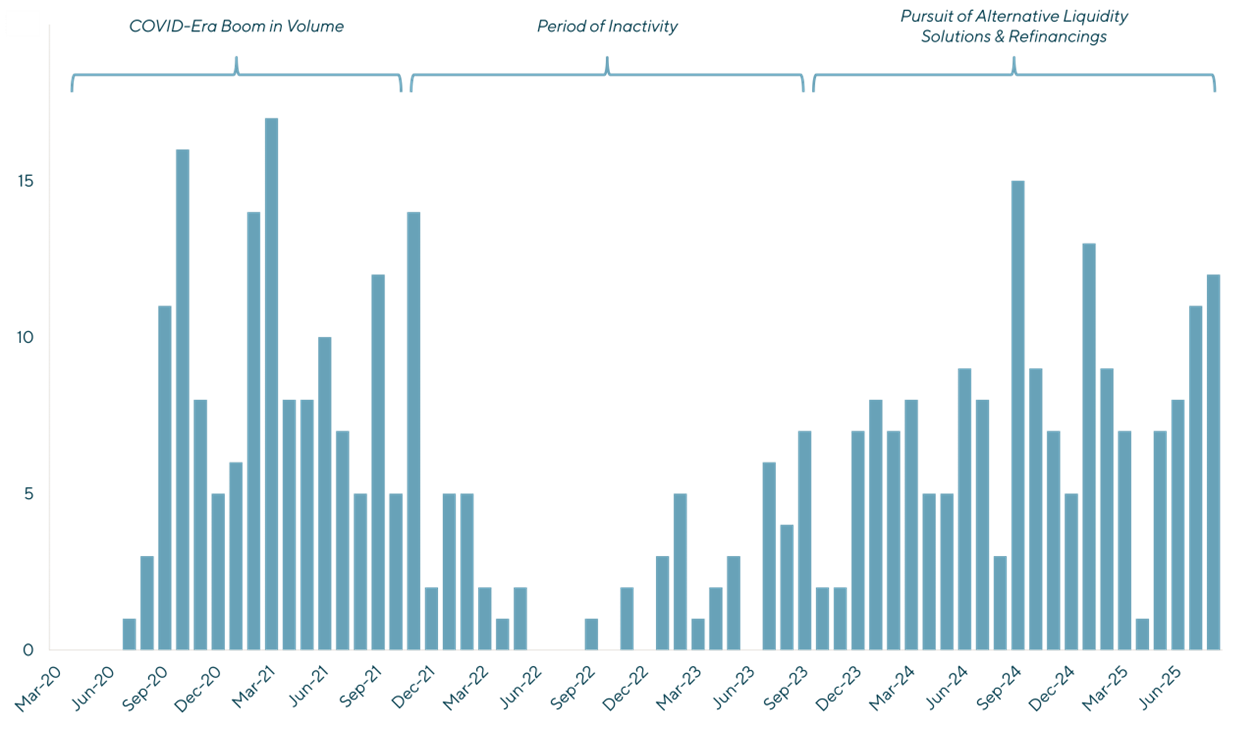

Fig.1: Number of dividend recapitalizations

Source: https://www.lincolninternational.com/perspectives/articles/dividend-recapitalization-activity-remains-robust/

Maturity Wall Looming for 2028

While current financing conditions continue to give the majority of borrowers ample room to refinance, an upcoming maturity wall that will see more than $1 trillion of speculative grade debt maturities hit in 2028 remains a concern.

Most of that debt relates to leveraged buyouts completed at a time when interest rates were much lower. While amend-and-extend transactions were down in 2025, we expect the maturity wall to fuel more of that activity in the coming year, with an ongoing flight to quality within private credit as lenders line up to support refinancings.

The proliferation of private capital providers in the market seeking footholds with sponsors means we are seeing these deals taking longer and due diligence processes lengthening. Borrowers seeking to refinance will need to be patient in 2026, particularly in distressed situations, and should think about strategies that enable them to hold onto assets for longer while dealing with the liquidity challenges that come with that.

Liability Management Transactions Take Hold

While the maturity wall will undoubtedly result in a wave of plain vanilla amend-and-extend transactions, the proliferation of more creative structures means that lenders are also preparing for opportunistic liability management transactions to the extent that sponsors cannot do regular refinancings.

At a time when fundraising is challenging and returning capital to investors is a priority, the ability of sponsors to contribute equity into struggling portfolio companies is constrained. That is driving evolution in the fund financing market, offering sponsors more flexibility to deploy capital into portfolio companies, but liability management transactions will continue to remain an important theme.

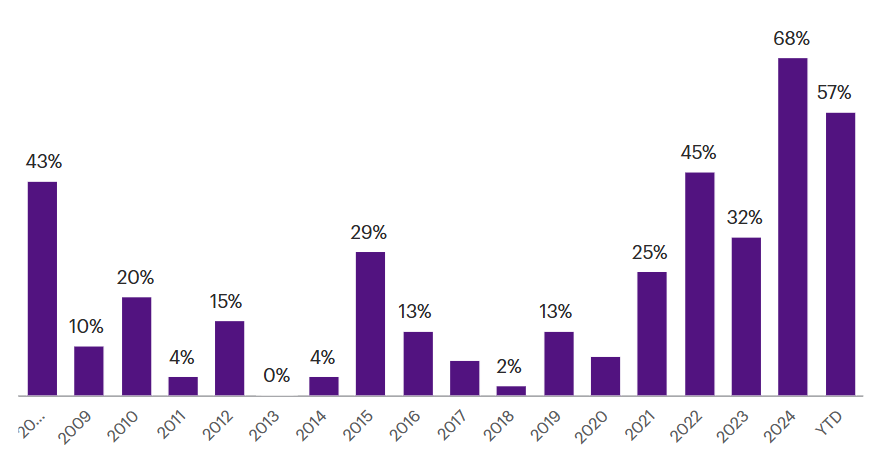

Fig.2: Liability management transactions as a percentage of total defaults, as of Aug 31, 2025