2026 Perspectives in Private Equity: LP Co-Investment in 2026: Key Structural Trends in Private Equity

This article is part of the “Perspectives in Private Equity” series.

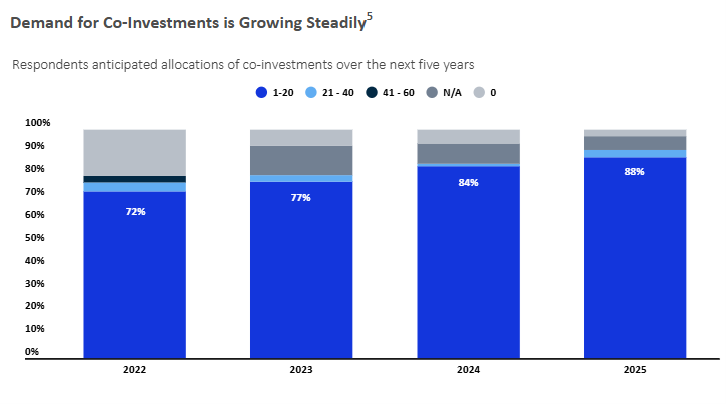

The number of limited partners looking for co-investment opportunities alongside their private equity GPs continues to grow and going into 2026 we have already seen an increase in co-investment activity. According to a survey by Adams Street, 88% of LPs intend to allocate up to 20% of their portfolios to co-investments between now and 2030, with demand having grown steadily over the last five years (see Fig.1).

Large institutional investors increasingly view co-investment access as a standard component of their relationship with private equity sponsors. Historically, co-investment opportunities were allocated on a discretionary basis and often limited to a sponsor’s largest or most strategic investors. Today, many LPs treat co-investment as a baseline expectation when committing capital to a fund. As a result, co-investment frameworks are increasingly discussed during fundraising and reflected in side letters or other investor arrangements. Sponsors are also providing greater transparency regarding allocation policies governing how co-investment opportunities are distributed among investors. In turn, this has resulted in a shift in trends shaping the co-investment landscape in 2026 and beyond.

1. Co-Investment as a Fundraising Tool

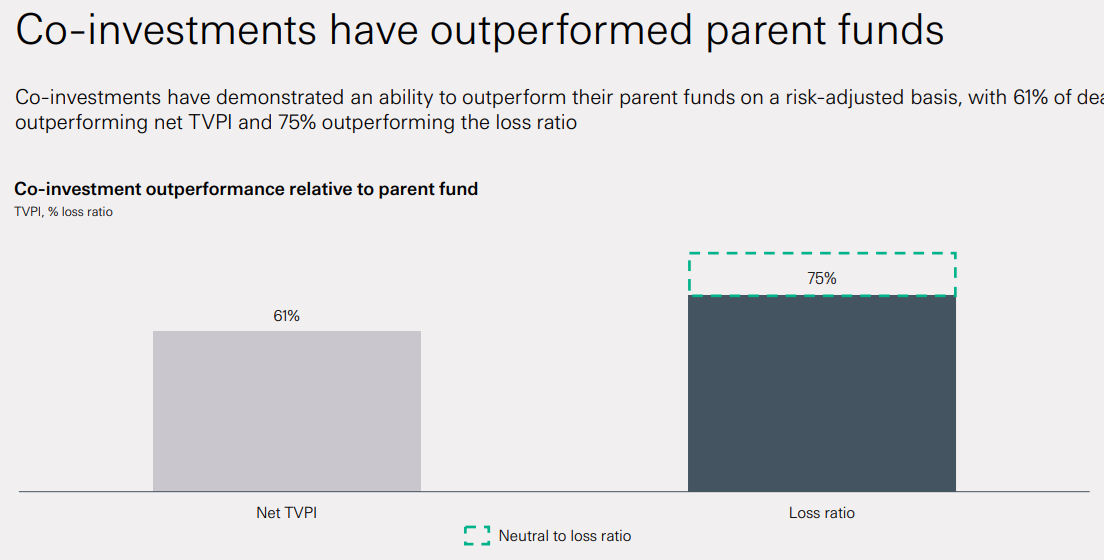

For both sides, the attractions of co-investment are manifold, with significantly reduced fees and carry typically making them a cost-effective way for LPs to increase exposure. Co-invests also allow LPs to strengthen their relationships with key sponsors, tighten alignment, gain enhanced visibility into deal processes and execute more control over portfolio management. Data from StepStone Group further suggests the majority of co-investment deals outperform parent funds (see Fig.2).

For GPs, co-investments now represent a key element of investor relations strategies and, in an environment where it is challenging and takes longer to raise primary capital, can be a good way to access money outside of the traditional fundraising cadence. Access to co-investment opportunities has become an important component of fundraising negotiations. Sponsors frequently offer priority access or allocation preferences to cornerstone or anchor investors, and some sponsors structure dedicated co-investment vehicles alongside their flagship funds.

2. Co-Investment as a GP Tool to Address Liquidity Pressures and Transaction Financing

The slower exit environment experienced across private markets in recent years has also contributed to the growth of co-investment activity. Further, in a market where massive deal sizes are becoming more common, bringing in a co-investor can help sponsors do bigger transactions without needing to team up with potential competitors or risk falling foul of fund concentration limits. At the same time, co-investment structures are appearing more frequently in connection with liquidity solutions, including continuation vehicles and other GP-led secondary transactions.

3. Expansion Across Private Markets Strategies

While co-investment historically developed in the context of buyout transactions, the model is increasingly being applied across a broader range of private-markets strategies. In particular, we have observed co-investment opportunities expanding in areas such as private credit, infrastructure and insurance-related asset management platforms.

This reflects the broader convergence of private capital strategies and the growing scale of institutional capital seeking direct exposure to underlying assets.

4. Bifurcation: Passive vs. Active LP Co‑Investors (and a New Focus on Continuation Vehicles)

What is increasingly evident in the 2026 co‑investment market is a bifurcation among LPs. Many LPs continue to pursue largely passive co‑investment strategies, acting as efficient term‑takers in sponsor‑led processes. At the same time, a growing cohort is seeking more active engagement—not only on economics, but also on governance and exit mechanics.

Historically, co‑investments were often structured with a contractual “tag” to the main fund, effectively aligning the co‑investment vehicle’s exit with the sponsor’s preferred path for the flagship fund. Drag‑along provisions reinforced that alignment by enabling the sponsor to compel the co‑investor to sell on substantially the same terms, preserving the sponsor’s ability to deliver a clean, single‑buyer exit.

However, as continuation vehicles and other GP‑led liquidity solutions have become a more established feature of the exit environment, LPs are increasingly asking whether it is appropriate for co‑investors to remain entirely at the mercy of sponsor discretion in affiliate or roll transactions. In practice, this has translated into more frequent negotiations around what happens to co‑investors in a continuation vehicle transaction—including whether the co‑investor has consent, consultation, election/opt‑out rights, or enhanced disclosure around process and conflicts.

In many co‑investment vehicles, the sponsor’s ability to pursue affiliate transactions is already permitted, subject to conditions. The shift in 2026 is that certain LPs are scrutinizing those conditions more closely and pushing for express provisions that clearly define co‑investor rights in the event of a continuation vehicle exit, rather than relying on broad discretion or generalized conflicts language.

Finally, this “active LP” posture often appears alongside a broader strategic evolution: for some institutions, co‑investment is increasingly viewed as a pathway to more direct investing—moving from passive participation to more proactive co‑investment, then to structured joint ventures, and in some cases toward independent deal leadership. Conversely, other LPs are doubling down on positioning themselves as high‑velocity co‑investment counterparties, building repeatable internal processes to partner efficiently with GPs without seeking bespoke control in every deal.

5. Increasing Customization

We see more customization of co-investment vehicles, with the increasing prevalence of programmatic cross-fund co-investment partnerships, separately managed accounts and custom-made co-investment pools. Such arrangements can be structured to permit the underlying LP to “opt in” or “opt out” of available opportunities based on a pre-agreed information memorandum presented by the sponsor, which avoids the need for protracted negotiation.

Tailored co-investment vehicles usually come with limited fee and carry arrangements that do not need to be negotiated every time, and there is an expectation that LPs will be able to respond quickly given that information and governance rights, economic terms and applicable investment parameters will have already been agreed. This gives LPs that have such arrangements in place with their sponsor partners a strategic advantage over other LPs or third parties – those unable to move fast to diligence on a co-underwriting or pre-signing basis will increasingly miss out.

More broadly, the due diligence involved on co-investments, and the regulatory analysis necessary to navigate Hart-Scott-Rodino (HSR) Act premerger antitrust notifications, CFIUS, FDI, merger control and other filings, means co-investors must increasingly sign equity commitment letters and other guarantees in order to participate.

What is clear, therefore, is that co-investment is no longer easily defined as a passive activity. As the range of LPs participating, and the diversity of approaches, continue to evolve, GPs need to prioritize offering high-quality opportunities and LPs with streamlined processes will have a competitive edge.

6. Regulatory and Structural Developments

Regulatory developments have also influenced the co-investment market. Recent signals from regulators suggest greater openness to streamlined exemptive frameworks for certain co-investment transactions involving regulated vehicles, which may facilitate more complex investment structures involving business development companies and other affiliated funds.

7. Increased Focus on Allocation Policies and Conflicts

As co-investment becomes more central to private equity dealmaking, sponsors and investors are paying closer attention to allocation frameworks and potential conflicts of interest. Key issues often addressed in fund documentation or internal policies include:

- how co-investment opportunities are allocated among investors,

- disclosure of potential conflicts,

- preferential rights granted through side letters, and

- governance considerations in GP-led transactions involving co-investors.

Sponsors are increasingly formalizing these policies to provide transparency and mitigate regulatory and investor scrutiny.

Fig. 1

Source: https://www.adamsstreetpartners.com/insights/2025-global-investor-survey/

Fig. 2