Brookfield-GGP Deal: Investors Face MLP vs. REIT Choice

By Stuart E. Leblang, Michael J. Kliegman, and Amy S. Elliott

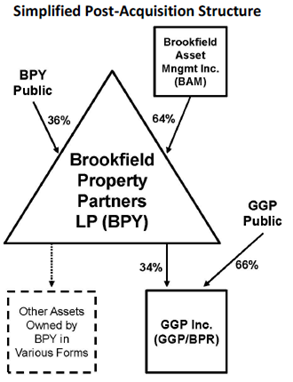

We have written about master limited partnership (MLP) Brookfield Property Partners LP’s (NASDAQ: BPY) (BPY) plans to acquire the real estate investment trust (REIT) GGP Inc. (NYSE: GGP) (GGP) in a deal that will give GGP shareholders the choice of receiving either all cash or a little bit of cash and either BPY units or shares of GGP (to be renamed BPR). As we noted in our April 20 report,[1]what is novel about this transaction is that it will be “structured with the intention of providing an economic return equivalent to BPY units, including identical distributions,”[2]to the REIT shareholders. Here, we discuss the structure that will arise from the acquisition, the mechanism created to achieve parity between the BPY units and the GGP shares, and the considerations that investors will face when choosing which position to take.

BPY issued its registration statement on May 2, 2018.[3] We continue to review all relevant information as it becomes publicly available and will update our reports as such new information warrants.

The Parity Mechanism

Perhaps the most interesting part of the resulting structure is the intended ongoing equivalence of two securities, each of which will be separately publicly traded. As indicated in our April 20 report, this equivalence is to be achieved through two features incorporated into the new Class A shares of GGP/BPR. One is a dividend right that tracks the amounts distributed on BPY units, and the other is a right to exchange BPR shares for BPY units or the dollar-value equivalent.

Specifics of the dividend are as follows:[4] Holders of BPR Class A shares (the shares not held by BPY or its affiliates) will be entitled to a dividend equal to the amount of distributions made by BPY to its unitholders. If a corresponding BPR dividend is not declared or paid contemporaneously with the BPY distribution, the BPR shareholders’ rights to the dividend will accrue and accumulate (without interest). To maintain economic parity between BPY units and BPR Class A shares, if BPY makes a distribution that is not matched by a BPR dividend, the 1:1 BPY-to-BPR convertibility will be adjusted to take into account the undistributed dividend to which the BPR shareholder is entitled.

Specifically, the original 1:1 conversion ratio will be proportionately increased by the shortfall amount such that the BPR shareholders’ units would be exchangeable for additional BPY units to reflect the unpaid dividend amount until it is paid, at which point the conversion ratio would be reset to 1:1. (The conversion ratio is also reset for various other events that would skew the proportional number of BPY units or BPR shares, e.g., distributions of equity, stock splits, or warrant distributions, as one would customarily find in options or convertible instruments.)

The more specific mechanics of the exchange right are as follows:[5] BPR Class A shareholders have the right at any time to require BPR to exchange their Class A shares for cash in amount equal to the fair market value of a like number of BPY units (subject to conversion adjustment to include unpaid dividends in the exchange). BPR is required to notify Brookfield Properties Inc. (BPI), an affiliate of Brookfield Asset Management Inc. (BAM), of the exchange request within one day. BPI may, in its sole discretion, elect to satisfy BPR’s exchange obligation by exchanging BPY units in a number determined under the conversion ratio described above for the BPR shareholder’s tendered BPR shares.

If after ten business days from the initial notice of exercise of the exchange right, the BPR shareholder has not exchanged its shares for cash or BPY units, it can exercise a secondary exchange right against BAM. BAM has entered into a rights agreement that requires it to maintain a collateral account to support its obligations with respect to the BPR shareholders’ secondary exchange right.[6] The right to recourse against BAM is ultimately what supports the intended value parity between BPR Class A shares and BPY units. We believe that the parties expect any exchanges by BPR shareholders to be effected by an exchange with BPI, as described above. It should also be noted that each of the means of effecting the exchange would be taxable.

Choice between BPY Units and BPR Shares

Surely, one of the primary reasons for implementing this dual-investment vehicle is to broaden the appeal of investing in real estate through BPY. Different investors will be afforded a choice that will allow for more efficient tax positions, and certain investors will be able to participate who otherwise might have been prohibited. For example, BPY and many of its subsidiaries are chartered in Bermuda, and many investors do not invest in non-U.S. entities or in vehicles established in what some perceive to be tax havens. Others do not invest through partnerships, and mutual funds generally make real estate investments only through REITs.

Tax considerations play a significant role in these decisions. Foreign investors, tax-exempt-investors, and individual U.S. investors each have different sensitivities, and we here discuss some of the advantages and disadvantages for potential investors in either BPY or BPR.

- S. Investors

- BPY Units: U.S. individuals and corporations that own BPY units will be subject to income tax on their allocable share of BPY’s taxable income. According to BPY’s SEC disclosures, between BPY and any of its investment real estate assets are multiple levels of foreign corporations.[7] Those corporations “block” income from being recognized by BPY before it is distributed up to BPY in the form of a dividend and prevent BPY and its partners from being treated as engaged in a trade or business.[8] Generally, a U.S. BPY unitholder would be subject to tax on dividends paid to BPY, whether or not distributed by BPY. Those dividends would be taxed at ordinary income rates to both U.S. individuals and corporations, and, for individuals, the 3.8 percent net investment income tax could apply. BPY unitholders would receive a Schedule K-1, rather than a Form 1099-DIV. Corporate BPY unitholders would not be entitled to a dividends received deduction for dividends from BPY’s foreign subsidiaries.

- BPR Shares: Individuals who own BPR shares would be subject to tax on ordinary and capital-gain dividends at ordinary and capital-gains rates, respectively. Additionally, an individual BPR shareholder would be entitled to the Tax Cuts and Jobs Act’s new 20 percent pass-through deduction (Section 199A) with respect to ordinary REIT dividends from BPR, which would effectively lower the tax rate on those dividends to a maximum of 29.6 percent, before the net investment income tax. (Corporations are not eligible for the Section 199A deduction.) Corporate BPR shareholders would be subject to the 21-percent income tax on BPR dividends and would not be entitled to a dividends received deduction.

- Foreign Investors

- BPY Units: Generally, a non-U.S. person would be subject to taxation on the income of BPY that is effectively connected with BPY’s U.S. trade or business. However, BPY takes the position that it is not engaged in a U.S. trade or business, which is consistent with the blocker structure discussed above.[9] Such a unitholder, not otherwise engaged in a U.S. trade or business, would be subject to a 30 percent U.S. withholding tax only on U.S.-source payments made to BPY, even if not distributed to the unitholders, in which case the unitholder would increase its BPY unit tax basis in the amount of undistributed income. We think it is unlikely that such U.S.-source payments will be made to BPY.

- BPR Shares: Foreign shareholders of BPR would be subject to a 30 percent withholding tax on ordinary dividends paid by BPR, subject to reduction by any applicable tax treaty. Because BPR is publicly traded, capital gain dividends paid by BPR to less-than-10-percent shareholders would be treated in the same manner as ordinary dividends. Finally, less-than-10-percent shareholders of BPR would not be subject to U.S. income tax upon a sale or exchange of BPR stock.

- Tax-Exempt Investors

- If held by a pension fund or tax advantaged retirement account, ownership of BPY units should not give rise to unrelated business taxable income (UBTI), because BPY is not engaged in a trade or business, and capital gains realized through BPY would not be taxable. Dividends paid by BPR would generally not create UBTI to tax-exempt investors.[10]

Below is a table that summarizes these points:

|

|

U.S. Investors |

Foreign Investors |

|---|---|---|

|

BPY |

• Individuals: 37 percent income tax on allocable share of dividends, interest, etc. from blockers to BPY, plus 3.8 percent net investment income tax • Corporations: 21 percent income tax on allocable share of dividends, interest, etc. from blockers to BPY: no dividends received deduction |

• Individuals and corporations: Subject to 30 percent withholding on allocable share of U.S. source FDAP (e.g., dividends and interest) income of BPY—unlikely there is any such income |

|

BPR |

• Individuals: 29.6 percent income tax on ordinary dividends: capital gain dividends taxed at 20 percent: both dividends subject to net investment income tax • Corporations: 21 percent tax on all dividends: no dividends received deduction |

• Individuals and corporations: Subject to 30 percent withholding tax on ordinary and capital gain dividends • No U.S. income tax on sale of BPR shares |

Preliminary Observations

The potential of the new structure to open up Brookfield’s real estate business to largely domestic REIT investors is likely worth the considerable creativity and grit that has gone into it. While ordinarily we would expect foreign investors to shy away from a partnership investing in U.S. real estate, it seems likely that BPY’s unusual current structure, which blocks U.S. source income, will continue to attract foreign investors, even as most domestic individual and institutional investors are drawn to the REIT.

As for whether the market will fully equate the value of BPR stock and BPY units, we will certainly have to wait and see.

[1] April 20, 2018, “Brookfield-GGP and the New MLP Tracking REIT”: see also our April 24, 2018, report, “GGP’s Pre-Closing Dividend—How Sure Is the Tax Treatment?”

[2] https://www.sec.gov/Archives/edgar/data/1496048/000114420418017000/tv489600_425.htm

[3] https://www.sec.gov/Archives/edgar/data/1545772/000119312518147184/d567992df4.htm

[4] See the Agreement and Plan of Merger and the Third Amended and Restated Certificate of Incorporation of GGP Inc., https://www.sec.gov/Archives/edgar/data/1545772/000114420418017984/tv489860_ex99-1.htm

[5] See the Agreement and Plan of Merger and the Third Amended and Restated Certificate of Incorporation of GGP Inc., https://www.sec.gov/Archives/edgar/data/1545772/000114420418017984/tv489860_ex99-1.htm

[6] See the Form of Rights Agreement,https://www.sec.gov/Archives/edgar/data/1545772/000114420418017984/tv489860_ex99-1.htm

[7] See BPY’s annual report, https://www.sec.gov/Archives/edgar/data/1545772/000154577218000003/bpy201720-f.htm

[8] Because BPY is not engaged in a trade or business, its unitholders are not eligible for the Section 199A deduction.

[9] See BPY’s annual report, https://www.sec.gov/Archives/edgar/data/1545772/000154577218000003/bpy201720-f.htm

[10] According to BPY’s most recent annual report, “The BPY General Partner intends to use commercially reasonable efforts to structure our activities to avoid generating income connected with the conduct of a trade or business (which income generally would constitute ‘unrelated business taxable income’, or UBTI, to the extent allocated to a tax-exempt organization). However, no assurance can be provided that we will not generate UBTI in the future. . . . The potential for income to be characterized as UBTI could make our units an unsuitable investment for a tax-exempt organization.”

Key Contacts