Sea Change: The SEC Makes Waves with New Proposed Climate Disclosure Rules

Sea Change: The SEC Makes Waves with New Proposed Climate Disclosure Rules

Sea Change: The SEC Makes Waves with New Proposed Climate Disclosure Rules

Key Points:

- On Monday, March 21, 2022, the SEC in a 3-1 vote proposed amendments to require public companies to provide certain climate-related information in their registration statements and annual reports. The amendments are intended to enhance and standardize certain climate-related disclosures in order to address investor demands for more consistent and comparable information about climate-related risks and impacts and supporting emissions disclosure.

- This release marks a significant step in the Biden administration’s transformation of the U.S. government’s response to climate change, as the administration proposes to leverage the SEC’s rulemaking authority as part of its whole of government approach to significantly enhance transparency around climate risks and claims.

- This Alert summarizes the proposed rules, provides information on the public comment period and offers recommendations on how to prepare for the potential new disclosure requirements.

Summary

Modeled in part upon the Task Force on Climate-Related Financial Disclosures (TCFD) and the Greenhouse Gas Protocol disclosure frameworks, the proposed amendments require disclosure of the following topics.

- Governance: Describe the board’s and management’s oversight and governance of climate-related risks.

- Climate-related Risks: Disclose the material impact or likely impact of identified climate-related risks on business and the consolidated financial statements, over the short-, medium- or long-term.

- Climate-related Impacts: Describe how identified climate-related risks have affected or are likely to affect strategy, business model and outlook.

- Internal Carbon Price: If used, disclose the internal carbon price and information on how it is set.

- Risk Management: Describe the processes for identifying, assessing and managing climate-related risks, and any integration into overall risk management.

- Transition Plans: For any transition plan adopted as part of climate-related risk management, describe the plan and include any relevant metrics and targets. If scenario analysis is used to assess resilience of the business strategy to climate-related risk, describe the scenarios used, as well as the parameters, assumptions, analytical choices and projected principal financial impacts.

- GHG Emissions Metrics Disclosure: Separately disclose direct greenhouse gases (GHG) emissions (Scope 1) and indirect GHG emissions from purchased electricity and other forms of energy (Scope 2), expressed both by disaggregated constituent GHG emissions and in the aggregate. Also disclose indirect emissions from upstream and downstream activities in a registrant’s value chain (Scope 3), if material, or if a GHG emissions target or goal that includes Scope 3 emissions has been set.

- Attestation of Scope 1 and 2 Emissions Disclosure: Provide, if an accelerated or large accelerated filer, an attestation report from a qualified outside service provider covering, at a minimum, the disclosure of Scope 1 and Scope 2 GHG emissions and certain related disclosures about the service provider.

- Targets and Goals: Disclose, if climate-related targets or goals have been published, (1)the scope of activities and emissions included in the targets, the time horizon for achievement and any interim target, (2) how such targets or goals are intended to be met and (3) the relevant data on progress made toward the targets or goals, with annual updates.

- Carbon Offsets: Disclose information about the use of any carbon offsets or renewable energy certificates (RECs) in achieving such targets or goals.

- Financial Statement Metrics: Provide climate-related financial statement metrics and related disclosure in a note to the company’s audited financial statements.

The proposed climate-related disclosures, both narrative and quantitative in form, are to be tagged in Inline XBRL and will be filed rather than furnished. For a more fulsome description of the proposed amendments, see Appendix A at the end of this alert.

Background

In 2010, recognizing the heightened interest in climate change matters, the U.S. Securities and Exchange Commission (SEC) published an interpretive release (the “2010 Interpretive Release”) that was intended to provide guidance to public companies regarding the SEC’s existing disclosure requirements as they apply to climate change matters. The 2010 Interpretive Release identified the “most pertinent non-financial statement disclosure rules” that could require disclosure related to climate change, including Item 101 of Regulation S-K – Description of Business, Item 103 of Regulation S-K – Legal Proceedings, current Item 105 of Regulation S-K (then Item 503(c)) – Risk Factors, and Item 303 of Regulation S-K – Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A). Since 2010, the SEC had remained largely silent on climate change until 2021, when it began to release a number of statements on, and take several notable actions related to, climate change disclosures and climate risks.

In February 2021, then-Acting Chair Allison Herren Lee issued a statement directing the Division of Corporation Finance to “enhance its focus on climate-related disclosure in public company filings.” After the creation of a Climate and ESG Task Force within the SEC’s Division of Enforcement to develop initiatives to proactively identify misconduct related to environmental, social and governance (ESG) issues, Acting Chair Lee issued a statement on March 15, 2021, requesting public input on 15 specific questions for consideration. Thousands of comments (over 600 unique comments) were submitted in response to the request. Concurrent with these actions, “Climate Change Disclosure” was added to the SEC’s official spring regulatory agenda. Then, in September 2021, a number of companies received comment letters regarding their climate-related disclosure or the absence of such disclosure as SEC Commissioners continued to discuss climate-related disclosure regulation and pressure mounted for the SEC to issue proposed rules.

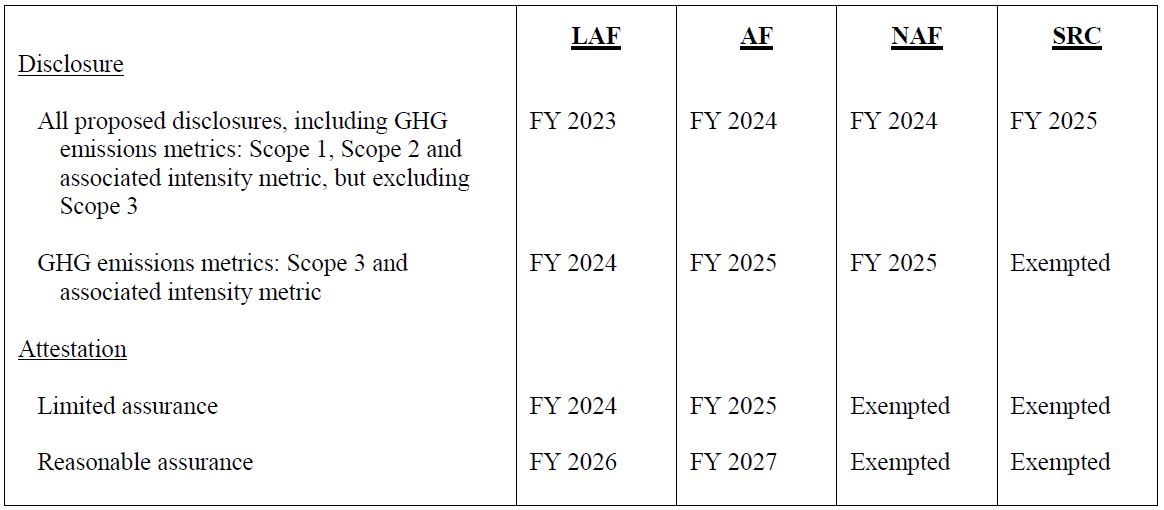

Compliance

The following table assumes that the proposed rules will be adopted with an effective date in December 2022 and that the filer has a December 31 fiscal year-end:

LAF—Large Accelerated Filer

AF—Accelerated Filer

NAF—Non-Accelerated Filer

SRC—Smaller Reporting Company

Impacted Forms

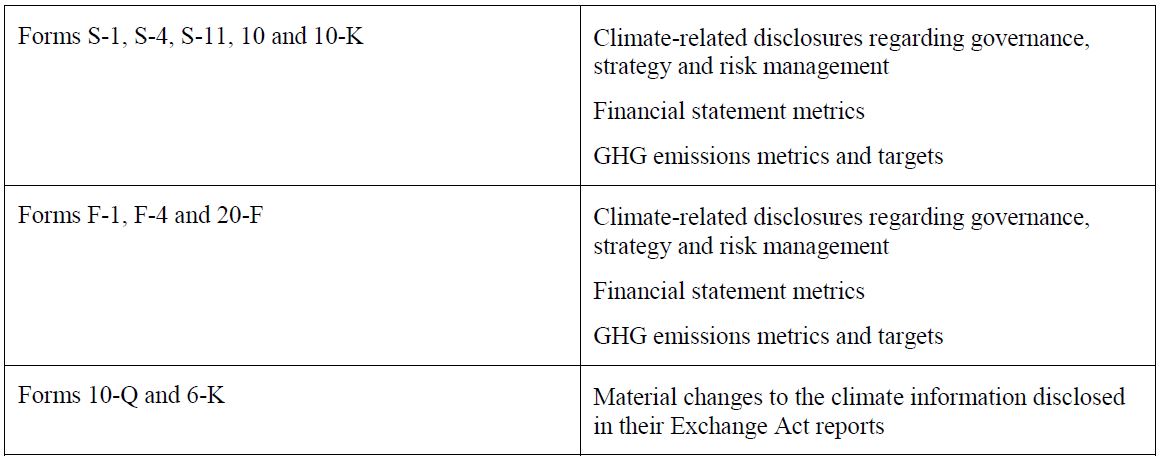

Each of Form S-1, Form F-1, Form S-4, Form F-4, Form S-11, Form 10, Form 10-K, Form 10-Q, Form 20-F and Form 6-K would be impacted by the proposed amendments.

Public Comment Period

The SEC is seeking comments by the 30th day after the release’s publication in the Federal Register or by May 20, 2022, whichever is later. Based on the degree to which stakeholders have been anxiously awaiting the publication of the proposed amendments, and lengthy statements made by the various Commissioners regarding such amendments, it is clear that the SEC expects significant commentary and engagement from actors from all sectors of the economy. In addition to a general request for comment on any aspect of the proposed amendments, the SEC solicited comments on over 200 specific topics in the release.

The SEC will take comments into consideration before issuing a final rule to be voted on by the Commissioners. Interested companies should evaluate areas of support or concern and consider filing comments before the conclusion of the comment period and/or directing advocacy and policy-maker outreach regarding necessary changes to be made before the rule is finalized.

Stakeholders should consider weighing in before the rule is finalized to preserve their right to challenge an unacceptable final rule. Regardless of the ultimate substance of the final rule, we anticipate that it will be litigated extensively in federal court—either challenging SEC for exceeding its authority by requiring such granularity in environmental and climate change disclosures or failing to go far enough on requiring such disclosures (or both). Commissioner Hester Peirce mentioned such challenges in her remarks voting against the proposed rules, and the SEC’s release includes commentary from the SEC attempting to defend such claims.

Criticism

In a lengthy dissenting statement, Commissioner Peirce made several critiques of the proposed rules asserting that: (i) existing rules already cover material climate risks; (ii) the proposed rules dispense with materiality in some places and distorts it in others; (iii) the proposal will not lead to comparable, consistent and reliable disclosures; (iv) the SEC lacks authority to propose the rules; (v) the SEC underestimates the cost of the proposal; and (vi) the proposed rules would hurt investors, the economy and the SEC. These criticisms mirror those voiced by opponents of the proposed rules.

Preparing for What’s Next

In preparation for the adoption of any final rules, U.S.-listed companies should take steps now in anticipation of these potential new requirements, including:

- Review Board and Management’s Role in Climate Oversight: Consider the board’s role in overseeing the governance and risk management of, and management’s role in assessing and managing, the company’s climate-related risks and opportunities. Consider board membership and expertise related to climate-related risks. Evaluate whether any related changes should be made to board committees or management positions, as well as committee charters.

- Evaluate Existing Disclosures: Many companies already release information about their GHG emissions and include climate-related risks and opportunities in their SEC reports and voluntary ESG or sustainability reports. Evaluate existing company disclosure and identify areas requiring lead time accounting or reporting infrastructure to comply with the proposed rules. Consider ways to leverage the methodology and processes already used to make existing climate-related disclosures portable to SEC reports.

- Revisit Climate Goals and Net Zero Plans: Consider whether the company has developed plans and milestones for achieving previously announced climate goals and net zero plans. Where applicable, look to prominent existing target-setting and disclosure frameworks, such as CDP (formerly, the Carbon Disclosure Project) for guidance on how to make accurate and sensible climate-related disclosures, including quantifying emissions throughout the value chain, where material.

- Assess Reporting Needs: Consider whether the company has sufficient in-house staff with relevant experience in evaluating climate-related risks and implementing related plans of action. Educate decision-makers and in-house counsel new to evaluating climate risk on how it may be material to a business, and ensure that the company considers the full range of climate-related risks, including both physical risks (e.g., loss or damage to property, sourcing and supply chain issues) and transition risks (e.g., business and regulatory changes that establish new market or legal challenges).

- Engage Experts: Consider whether to engage additional third-party climate consultants and counsel to evaluate the company’s climate risk profile and advise on scenario analysis methodologies, annual climate-related disclosure and the eventual anticipated need to obtain an attestation report covering emissions disclosures.

- Begin Dialogue with Auditors: Discuss the proposed amendments with your independent auditor.

This release marks a significant step in the Biden administration’s transformation of the U.S. government’s response to climate change, as the administration proposes to leverage the SEC’s rulemaking authority as part of its whole of government approach to significantly enhance transparency around climate risks and claims.

Authors