A hedge agreement is a contractual device used to lock in a predictable, per-unit price against commodity price fluctuations; however, although a hedge agreement transfers price risk away from the facility owner, volumetric (or production) risk often remains with the facility owner.

There are two basic types of hedges in the Texas market, distinguished by how the hedge is settled, and each type handles production risk quite differently. One type, a fixed-shape hedge, settles pursuant to a set megawatt hour (MWh) schedule that is independent of the actual megawatt hour production from the facility. The second type, a percentage-offtake hedge, settles pursuant to a percent (sometimes 100%) of the megawatt hour production from the facility. Facilities that lost their production capabilities due to the Texas storm generally faired neutrally if they had percentage-offtake hedges because no energy was settled against ultra-high market prices. Conversely, the facilities with a fixed-shape hedge were the ones that generally fared poorly because they were forced to settle (in accordance with their set MWh schedule) against such high market prices without the benefit of receiving these high market prices through their physical production of MWhs.

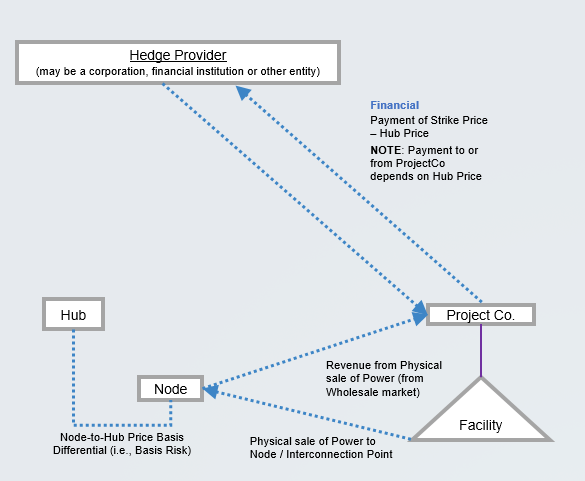

The following chart demonstrates a typical hedge arrangement (whether it is a fixed-shape or percentage-offtake hedge) (note, for simplicity, this shows a financially settled hedge, but the concept equally applies to a physically settled hedge).

Hedge documents primarily capture the arrangement between the project company and the hedge provider, which is illustrated in the top half of the chart above. Revenue received from the wholesale market, based on the facility’s actual production, is what underpins the ability of the project company to pay the hedge provider through financial settlement (or to schedule and deliver energy at the hub, if this is a physically settled transaction). This wholesale revenue is represented in the bottom half of the chart. In a fixed-shape hedge, the transaction between the project company and hedge provider continues, regardless of whether the project company is receiving revenue from its actual production. In a percentage-offtake hedge, the settlement between hedge provider and project company is dependent upon (and directly correlated to) the amount of production from the facility.

When the hub price reaches $9,000 per MWh and the facility shuts down due to icy conditions, a fixed-shape hedges continues settlement of the hedge arrangement, based on the $9,000-per-MWh price and predetermined settlement quantity; however, a percentage-offtake hedge will not settle because the quantity will be zero. As a result, the project company with a fixed-shape hedge must pay the hedge provider the difference between $9,000 and the strike price when it has no underlying revenue coming in, which is the primary cause of the liquidity crunch many facilities in Texas with hedge offtake agreements are facing (that is, project companies with fixed-shape hedges).

While renewable energy hedges in Texas are, as a whole, lumped together as poor performers in the recent Texas winter storm, the facilities with percentage-offtake agreements emerged (generally) unscathed while the facilities with fixed-shape hedges generally are hurting.

{kind=link}